Lathe & Milling Machine Financing: Equipment Loans, Leases & SBA Programs

Lathes and milling machines—manual and CNC—cost $20,000–$250,000+ new depending on size and type, typically 25–45% less used. Spread the cost with equipment financing. Decisions in 24–48 hours for qualified applications. Manufacturers nationwide.

- Equipment financing decisions in 24–48 hours

- Loans and leases for manual and CNC lathes and mills

- Typical terms 36–72 months; SBA to 7–10 years

- Credit 600+; 0–20% down payment

Lathe & Mill Financing at a Glance

Why Lathe & Mill Financing Makes Sense for Manufacturers

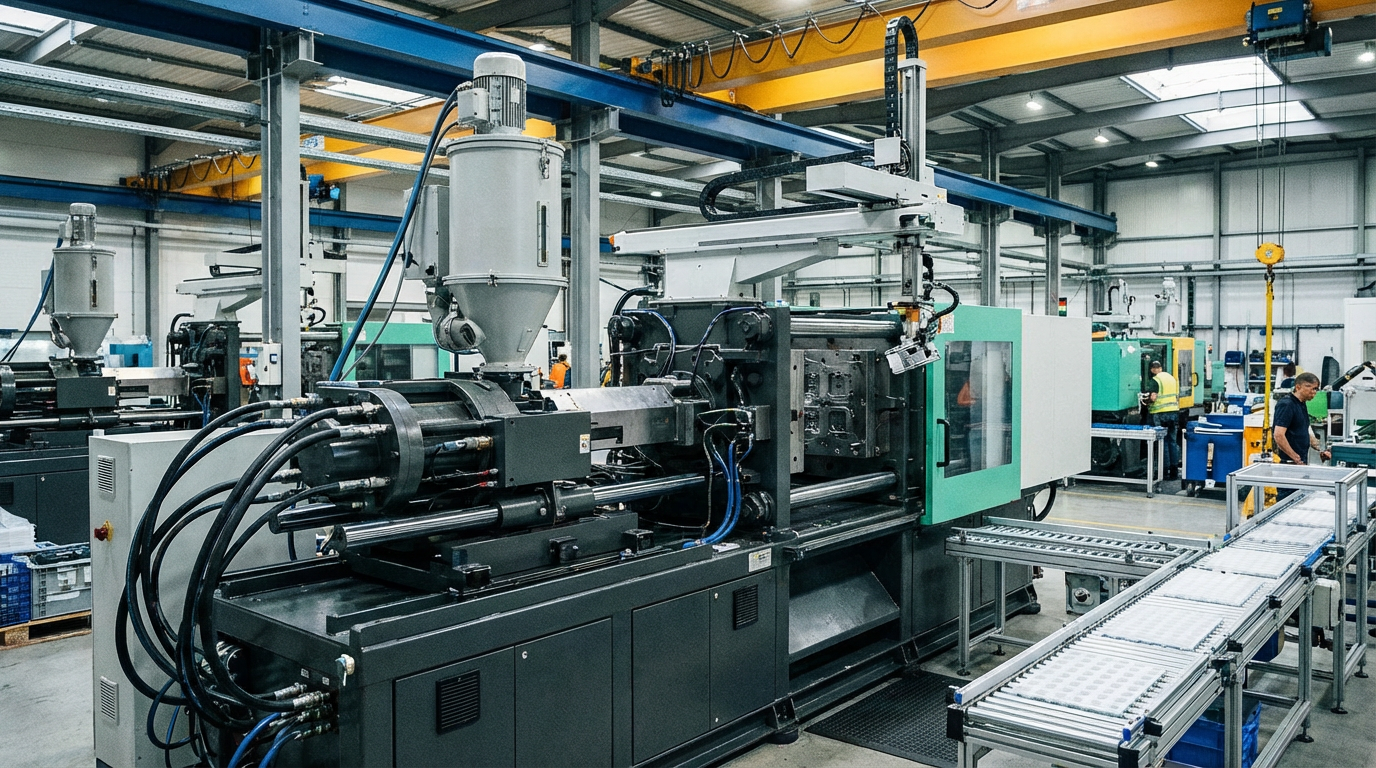

A lathe rotates a workpiece while cutting tools shape it—used for turning, boring, threading, and facing. A milling machine holds the workpiece stationary while rotating cutters remove material—used for milling, drilling, and boring. Both come in manual and CNC versions. With new lathes and mills costing $20,000–$250,000+ depending on type and size, paying cash ties up capital you need for payroll, materials, and growth.

Job shops and manufacturers rely on lathes and mills for precision parts. Equipment financing spreads the cost over the machine's useful life. Haas, Mazak, Okuma models hold value. Manufacturing lenders often offer terms of 36–72 months or longer. Tax benefits—Section 179 and bonus depreciation—reduce the true cost. Apply now to get matched with lenders who specialize in manufacturing equipment financing.

What Are Lathes and Milling Machines?

A lathe rotates a workpiece while cutting tools shape it—used for turning, boring, threading, and facing. A milling machine holds the workpiece stationary while rotating cutters remove material—used for milling, drilling, and boring. Both come in manual and CNC versions. Manual machines are operator-controlled; CNC use programmed instructions for repeatable precision. Lathes range from bench lathes to large engine lathes. Milling machines include vertical mills, horizontal mills, and knee mills. Essential for job shops, machinists, and manufacturers.

Why Lathe & Mill Financing Is Different

Manual and CNC lathes and mills serve job shops and manufacturing. Haas, Mazak, Okuma common. Lenders treat them like CNC equipment. Job shops often have project-based revenue. Used lathes and mills 5–10 years old are financed. Tooling can be bundled.

Lathe & Mill Financing Options

Several financing structures work. Choose based on cash flow, tax situation, and ownership goals.

Equipment Loans

Borrow, make fixed monthly payments, own the machine when paid off. 0–20% down, terms 36–72 months. Rates 6–15%. Ideal for long-term use. Equipment financing.

Equipment Leasing

Lower monthly payments. At lease end, return, purchase at fair market value, or upgrade. Loan vs lease.

SBA Loans

SBA 7(a) can finance lathes and mills with longer terms and lower down payments. Approval 30–60+ days. Best for established manufacturers.

Working capital loans suit operating expenses. Use equipment financing for the lathe or mill to secure better rates tied to the asset. Working capital.

How Much Do Lathes and Milling Machines Cost?

New manual lathes range from roughly $20,000–$80,000. New manual mills (knee mills, bed mills) typically cost $25,000–$75,000. New CNC lathes range from roughly $80,000–$200,000+; CNC mills and machining centers from $80,000–$250,000+. Used lathes and mills typically cost 25–45% less. A 5-year-old CNC lathe might run $50,000–$120,000. Older manual machines can start around $5,000–$25,000. Many lenders finance used equipment up to 7–10 years old. Obtain a written quote. Estimate payments.

Lathe & Mill Financing Rates and Monthly Payments

Rates typically range 6–15%. Terms run 36–72 months for standard equipment financing; SBA extends to 7–10 years. A $75,000 CNC lathe at 8% over 60 months would run roughly $1,520/month. Typical rates. Financing calculator. Down payment requirements vary.

Requirements to Finance a Lathe or Mill

Lenders evaluate several factors. Meeting these improves approval odds.

Credit: Most lenders look for 600+. Credit requirements. Some programs work with 580+ when revenue and down payment are strong. Documentation: Bank statements, tax returns, profit & loss, equipment quote. Customer contracts and backlog help. What lenders look at.

What to Have Ready Before You Apply

Gather: 3–6 months of business bank statements, tax returns (business and personal if required), recent profit and loss, equipment quote, business formation documents, and basic info. Lenders may ask for a voided check for ACH.

When to Apply for Lathe or Mill Financing

Apply when you have a clear equipment need, a written quote, and financials showing your business can support the payment. Apply before you need the machine—approval often takes 1–5 days. Early application gives you time to compare. Axiant Partners matches businesses with lenders—submit once, receive offers typically within 24–48 hours.

Tips to Get Approved

- Improve your credit score. Pay down balances, correct errors, avoid new credit.

- Provide strong revenue documentation. Clean bank statements and customer contracts strengthen your application.

- Consider used equipment. Quality used lathes and mills cost significantly less. Inspect ways and spindle.

- Make a larger down payment. Reduces lender risk.

- Choose equipment with strong resale value. Major brands hold value better.

- Work with a broker. Apply through Axiant to connect with multiple lenders.

Common Mistakes to Avoid

- Skipping the equipment quote. Lenders need it.

- Applying with incomplete financials. Missing documents cause delays.

- Focusing on rate alone. Terms, fees, flexibility matter.

- Waiting until the last minute. Rush approvals may limit options.

- Ignoring used equipment. Quality used lathes and mills can cost 25–45% less.

Why Businesses Finance Lathes and Mills Rather Than Pay Cash

Paying cash ties up working capital. Financing spreads the cost, matches expenses to revenue, and preserves liquidity. Equipment loans and leases offer tax benefits—Section 179 and bonus depreciation; lease payments as operating expenses. Many manufacturers prefer to finance to keep reserves.

How the Lathe & Mill Financing Process Works

Standard approval takes 1–5 business days. Day 1: submit application and documents. Days 2–3: lender review. Day 4–5: approval, documentation, funding. Funds go to the seller; you take possession.

Get a Quote & Apply

Obtain a written quote. Complete one application—we submit to multiple lenders.

We Match You With Lenders

Our team identifies lenders whose programs fit your lathe or mill purchase.

Review & Approve

Equipment financing often requires minimal docs. Decisions in 24–48 hours.

Funding & Closing

Once approved, sign documents. Funds go to the seller. You take possession.

Related Manufacturing Equipment

Browse financing for similar equipment. One application, we match you with lenders.

Lathe & Mill Financing FAQ

Can you finance a used lathe or mill?

Yes. Many lenders finance used lathes and milling machines, typically 7–10 years old or newer. Hours, condition, and brand affect approval.

What credit score is required?

Most lenders look for 600 or higher. 680+ qualifies for the best rates.

Manual vs CNC—does it affect financing?

Lenders finance both. CNC equipment typically costs more and may qualify for longer terms. Price and condition matter more.

How long does approval take?

1–5 business days for equipment loans and leases. SBA adds 30–60+ days.

Is leasing better than buying?

It depends. Leasing offers lower payments and easier upgrades. Buying builds equity. Compare both based on cash flow. Equipment loan vs lease.

What documents are needed?

3–6 months of bank statements, tax returns, profit and loss, equipment quote, and business formation documents.

More Equipment Financing Resources

Ready to Finance Your Lathe or Milling Machine?

Applications are reviewed within 24–48 hours. We match manufacturers with lenders who specialize in manufacturing equipment financing.

Get Matched for Lathe & Mill Financing