Why a business line of credit draw gets declined: utilization rules, covenant-like triggers, stale financials, and how to fix each. Common reasons: covenant breach (e.g., DSCR, tangible net worth), material adverse change in your financials, drawing over available credit, or the line is under annual review and not yet renewed.

1. Covenant Breach

Most lines of credit have financial covenants—debt service coverage ratio (DSCR), tangible net worth, leverage ratio, or similar. If you’ve breached a covenant, the lender can decline draws until you’re back in compliance or they grant a waiver. Covenants are typically tested at each draw or periodically (e.g., quarterly). A breach gives the lender the right to stop advances.

Fix: Know your covenants. Monitor them before you request a draw. If you’re close or in breach, get back in compliance or contact the lender for a waiver before drawing. See loan covenant breaches: how to avoid them and what to do if at risk. Don’t assume the lender will overlook a breach—they often won’t.

2. Material Adverse Change

Line agreements typically require that no “material adverse change” has occurred in your business or financial condition. If revenue has dropped sharply, you’ve lost a key customer, or there’s litigation or other risk the lender learns about, they may decline draws. The lender doesn’t have to prove you’re in default—they can refuse advances if they believe your ability to repay has materially worsened.

Fix: If you’ve had a material change, consider informing the lender before you draw—especially if they might find out anyway (e.g., through a credit bureau or news). Proactive communication can sometimes preserve the relationship. If the change is temporary, provide a narrative and supporting data. See why business lines of credit get cut or revoked.

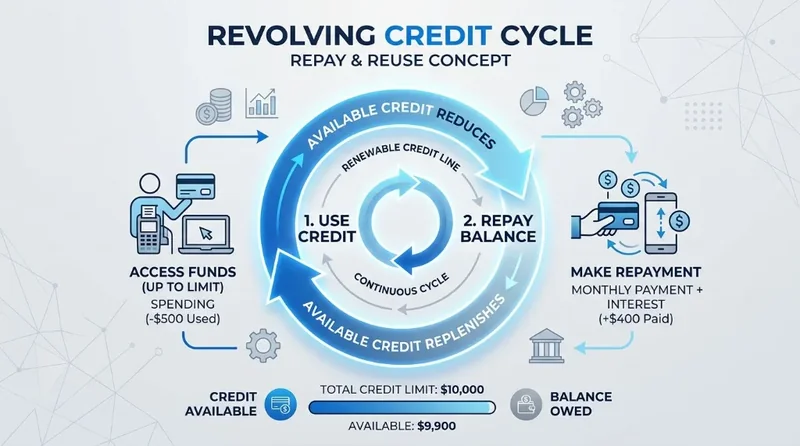

3. Over Available Credit

You can only draw up to your available credit—the line limit minus current balance. If you’re requesting more than what’s available, the draw will be declined. Some borrowers miscalculate, or the available amount has changed (e.g., a payment hasn’t posted, or the lender reduced the line).

Fix: Check your available balance before requesting a draw. If you need more than you have, pay down the line to free capacity, or ask the lender for a limit increase. See why your line of credit limit is too low for how to qualify for more. Don’t assume you can draw up to the full limit if you have an outstanding balance.

4. Line Under Annual Review

Many lines require annual renewal or review. During that period, the lender may restrict or suspend draws until they complete the review and renew. If your line is coming up for renewal and you haven’t submitted the requested financials or completed the process, draws can be declined.

Fix: Respond to annual review requests promptly. Submit documents needed for business line of credit as soon as the lender asks. Don’t wait until you need to draw—complete the review before you need the money. If the lender is slow, follow up; don’t assume it’s automatic.

5. Default or Event of Default

If you’re in default—missed payment, covenant breach, insolvency, or other event of default—the lender can decline all draws. They may also accelerate the line (demand full repayment). Default doesn’t have to be payment-related; it can be a covenant breach or a representation that’s no longer true.

Fix: Avoid default. Make payments on time. Stay within covenants. If you’re in default, remedy it as soon as possible and ask for a waiver or forbearance. See loan covenant breaches: how to avoid them. If the lender has accelerated, get legal advice—you may need to refinance or negotiate.

6. Use of Funds Restriction

Some lines restrict how you can use the funds—e.g., working capital only, no acquisitions or dividends. If the lender discovers or believes you’re using draws for an ineligible purpose, they can decline future draws or call the line. They may also ask for certification of use at each draw.

Fix: Read your agreement. Use draws only for permitted purposes. If you need funds for something that might be restricted, ask the lender in advance. Don’t assume “working capital” covers everything—some agreements are specific. See business line of credit requirements.

7. Lender Policy or Portfolio Change

Sometimes the decline isn’t about you specifically—the lender may have tightened credit policy, reduced exposure to your industry, or is managing portfolio concentration. They may decline draws even when you’re in compliance. This is less common but happens during economic stress or when lenders reposition.

Fix: Ask why the draw was declined. If the lender cites policy or portfolio reasons, you may need to find alternative financing. See why business lines of credit get cut or revoked. Get matched to reach other lenders if your current line is no longer reliable.

What to Do Right Now

If your draw request was declined: (1) Ask the lender for the specific reason. (2) If it’s a covenant breach, get back in compliance or request a waiver. (3) If it’s capacity, pay down the line or request an increase. (4) If it’s annual review, complete the review. (5) If the lender has changed policy or is cutting the line, explore alternatives. For red flags before you sign, see red flags in line of credit offers. When you need a new or backup line, get matched.

Frequently Asked Questions

Why would my line of credit draw request be declined?

Common reasons: covenant breach (e.g., DSCR, tangible net worth), material adverse change in your financials, drawing over available credit, or the line is under annual review and not yet renewed. Fix by staying within covenants, keeping the lender informed of material changes, and ensuring you have available capacity.

Can a lender decline a draw on an existing line of credit?

Yes. Most lines have conditions to each draw: no default, no covenant breach, no material adverse change. If any of those exist, the lender can decline. See why business lines of credit get cut or revoked.

What should I do if my draw request is declined?

Ask the lender why. If it's a covenant breach, get back in compliance or negotiate a waiver. If it's capacity, pay down the line or wait. If the line is under review, complete the review. See documents needed for business line of credit for annual review requirements.