Reverse Consolidation Explained

How reverse consolidation replaces several daily debits with one lower weekly payment — and who it fits.

Read moreMultiple cash advances and unsecured loans draining your account every day or week? We help you combine them into a single, lower payment—then match you with the lender or consolidation partner that fits. One conversation, no obligation.

Tell us about your current advances and loans. A specialist reviews your positions and maps the realistic ways to one lower payment—no obligation, and no hard credit pull to get started.

A specialist will review your positions and reach out, usually the same business day.

Your reference number:

Want to talk now? Call (561) 268-0465

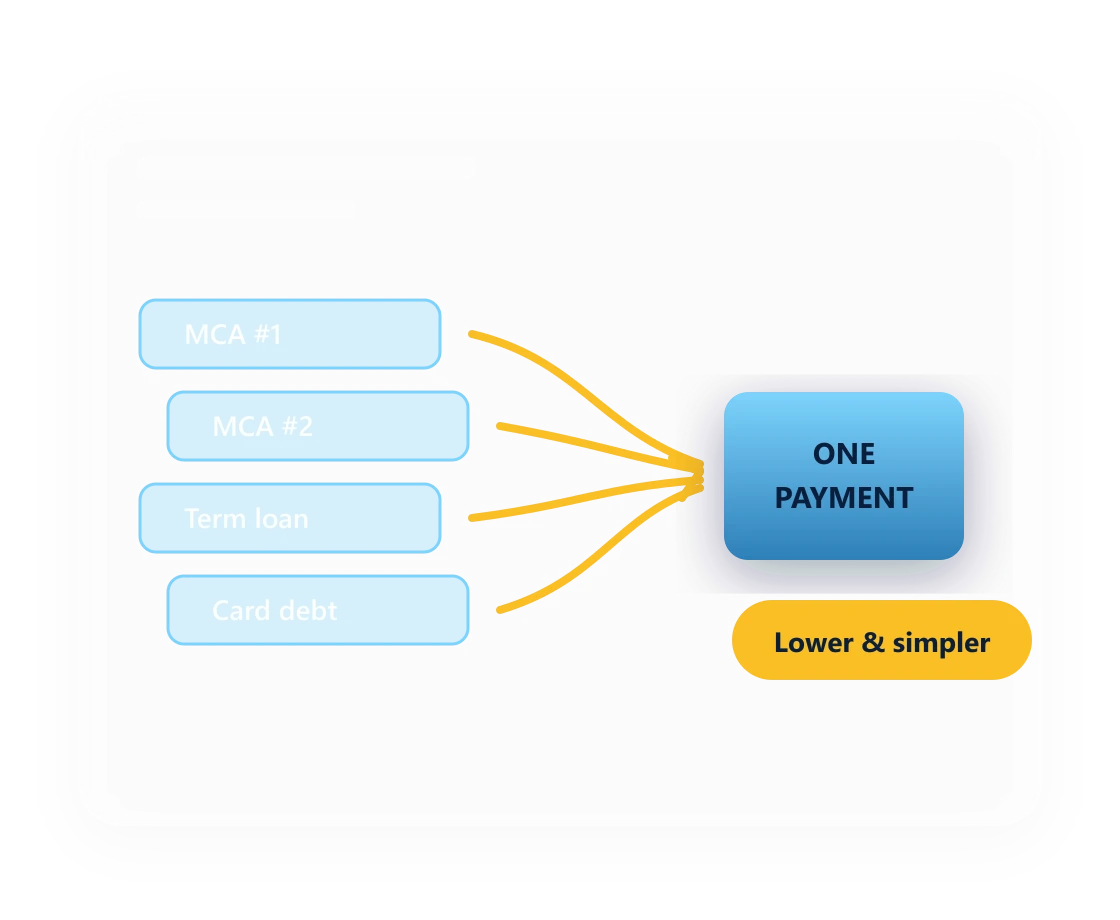

Business debt consolidation replaces several debts with one new facility and one payment. For a business carrying stacked merchant cash advances, that means ending multiple daily or weekly ACH debits and moving to a single scheduled payment. Whether it is available depends on your revenue, the positions outstanding, and whether you own assets that can secure the new facility.

Business debt consolidation combines several business debts into a single new facility with one payment. Instead of juggling multiple loans, merchant cash advances, and card balances with different due dates and rates, you refinance them into one loan or line—ideally at a lower rate or a longer term—so the combined payment is smaller and easier to manage. It is a refinancing strategy that keeps your accounts in good standing, not a settlement of debt for less than you owe.

Axiant Partners reviews the debt you carry and connects you with the lender or consolidation partner that actually fits. We are a matching and advisory service—we don't lend, settle debt, or give legal or tax advice ourselves. If you are already badly behind and consolidation isn't realistic, we will tell you and point you to other debt-relief paths. Otherwise, get a free consolidation review.

If two or more of these are competing for the same cash, they're candidates to fold into one payment.

Two, three, or more MCAs with overlapping daily or weekly debits—often consolidated or reverse-consolidated into a single, lower weekly payment.

Steep factor-rate or high-APR balances that can be refinanced into a longer, more predictable term loan.

Revolving lines of credit and business card balances rolled into one fixed payment instead of several minimums.

Most unsecured obligations weighing on cash flow can be reviewed for consolidation into cheaper, better-structured working capital.

Share your balances, the advances or loans you carry, and your combined daily or weekly payment. It takes about a minute and there's no hard credit pull to get started.

A specialist looks at your positions and cash flow and maps the realistic consolidation options—one term loan, a reverse consolidation, or better-priced capital.

We connect you with the lender or consolidation partner that fits, so you are talking to the right provider instead of dialing for quotes.

Replace the stack of overlapping debits with a single, more manageable payment—and get back to running the business.

Consolidation is worth a look when the debt itself has become the problem. Common signals include:

If two or more sound familiar, a review is worth it. Read about the How to Get Out of Bad Business Debt before you decide.

Enter your total balance owed across all advances and the combined weekly payment you send now to estimate a single, lower weekly payment and the monthly cash you could free up. Illustrative only — for real numbers, get a free review.

Illustrative estimate based on a typical 40–60% payment reduction. Not a quote, approval, or offer of credit.

Get a free consolidation review →Consolidation is not the only route. Here's how it compares to the alternatives a specialist will weigh with you.

Not sure which fits? Use our financing calculator to estimate payments, or get matched and let a specialist map it out.

Axiant matches; lenders and partners fund. Axiant Partners is a financing match and advisory service. Consolidation loans and refinancing are provided by independent lenders and partners—not by Axiant. We help you understand the options and connect you with the right provider.

Results are never guaranteed. Not every business or debt type qualifies for consolidation. No lender is required to approve financing. Any figures, ranges, or timelines on this page are illustrative examples, not offers or quotes.

Consolidation is not debt settlement. Consolidation refinances what you owe into one payment and keeps accounts in good standing. Settlement—resolving a balance for less than owed—is a different path that can lower credit and have tax consequences. If that's what your situation needs, see our debt-relief page.

This isn't legal, tax, or financial advice. The information here's general and educational. Consult a qualified attorney, accountant, or financial advisor before entering any consolidation or refinancing arrangement.

Business debt consolidation combines several business debts into a single new facility with one payment. Instead of juggling multiple loans, merchant cash advances, and card balances with different due dates and rates, you refinance them into one loan or line, ideally at a lower rate or a longer term, so the combined payment is smaller and easier to manage. It is a refinancing strategy that keeps your accounts in good standing, not a settlement of debt for less than you owe.

Often, yes. Businesses with multiple merchant cash advances draining overlapping daily or weekly debits may be able to consolidate or refinance those positions into a single, lower payment, sometimes through a term loan or a reverse consolidation. Eligibility depends on your revenue, the number and size of the positions, and the underlying agreements. A specialist can review your positions and outline realistic options.

Common candidates include stacked merchant cash advances, high-cost short-term loans, business lines of credit, business credit card balances, and other unsecured business debt. The goal is to replace several high-cost or overlapping payments with one more manageable payment. Whether a specific balance can be folded in depends on the lender and your overall profile.

Consolidating or refinancing into a new loan that you pay on time generally supports your credit, because you keep accounts current and reduce the number of open obligations over time. This is different from debt settlement, which resolves balances for less than owed and can lower credit and create tax consequences. Outcomes vary by lender and your situation, and nothing is guaranteed; consult a qualified advisor about your specific case.

Axiant's matching and review service is free to you. We are compensated by our lending and partner network. We help you understand your consolidation options and connect you with the lender or partner that fits your situation. Axiant Partners is a financing match and advisory service and does not provide legal, tax, or debt-settlement services itself.

Most consolidation programs look at your monthly revenue, time in business, the size and number of existing positions, and your credit. Businesses with steady revenue that still service their debt are the strongest candidates for a lower-cost consolidation. If you are already badly behind, a different relief path may fit better. The fastest way to know is a free, no-obligation review of your specific positions.

Go deeper on stacked-advance situations and the routes back to one payment.

How reverse consolidation replaces several daily debits with one lower weekly payment — and who it fits.

Read moreWhy a freeze happens, what to do in the first 24–48 hours, and the routes to get a business account released.

Read moreHow mediation restructures stacked, distressed debt into one consolidated, cash-flow-aligned payment.

Read moreCompare consolidation, restructuring, and settlement when the debt itself has become the problem.

Read moreIf stacked advances and high-cost debt are choking your cash flow, there is usually a way to one lower payment. Tell us about your debt once and we will review your options and match you with the right lender or consolidation partner—no cost for the match guidance, no obligation.