What is keeping you from refinancing business debt: eligibility blockers, documentation gaps, and how to fix them quickly. Common barriers: credit below the new lender's bar, cash flow or bank statements weakened by current debt payments, too much total debt to support a new loan, or payoff restrictions in existing contracts.

1. Credit Below the Refinance Lender’s Bar

Refinance lenders still underwrite you. If your credit has slipped since you took the original debt, or the new lender wants a higher score than you have, you may not qualify. Fix: check your report, dispute errors, and pay down revolving balances. Give it 2—3 months of clean behavior. Target lenders that work with your score tier or specialize in consolidation. See business loans for bad credit for options.

2. Cash Flow or Statements Weakened by Current Payments

Daily MCA remittance or high loan payments can depress bank balances and make your revenue look weaker. Lenders evaluating you for refinance see those statements and may decide you can’t support a new payment. Fix: clean up your banking for 2—3 months where possible—avoid overdrafts, keep one primary account, and show consistent deposits. If you can pay down one advance to reduce daily remittance before applying, that can help. Some lenders specialize in refinancing businesses with current MCA or high-cost debt.

3. Too Much Total Debt to Support a New Loan

Refinance means the new lender pays off the old one(s) and you pay the new lender. They need to see that your revenue supports the new payment. If your total debt load is already high, they may decline or offer less than you need to pay off everything. Fix: get payoff amounts for all existing debt. Apply for a refinance amount that covers payoffs and fits your cash flow. You may need to refinance in stages—highest-cost first—or pay down one advance before applying. See how much you can qualify for with a working capital loan.

4. Payoff Restrictions or Timing

Some MCA or loan contracts have prepayment restrictions, payoff fees, or notice requirements. The refinance lender may need to coordinate payoff with the existing funder. Fix: read your contracts and know the payoff process. Get a payoff quote and timeline from each existing lender. Share that with the new lender so they can structure the refinance and fund at closing. For red flags in high-cost agreements, see red flags in MCA agreements.

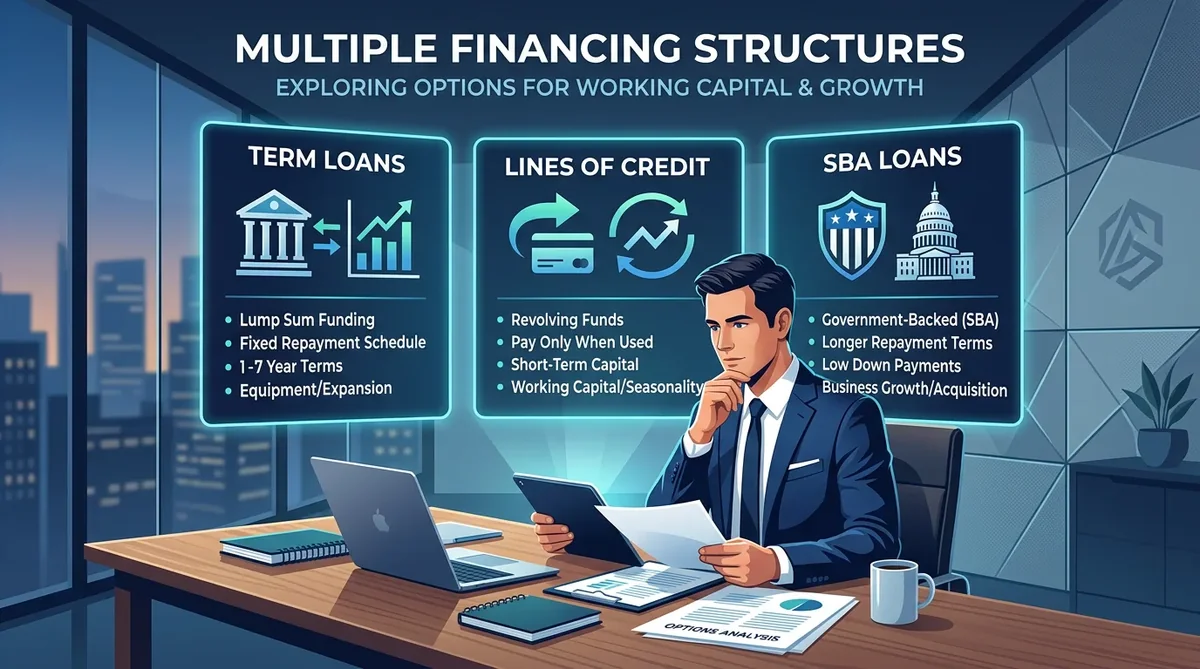

5. Choosing the Wrong Refinance Product

Refinancing into another high-cost or short-term product doesn’t solve the problem. Fix: aim for a term loan or line of credit with a lower effective rate and a fixed monthly payment so you have a clear payoff path. Compare total cost (APR, fees, term) and avoid refinancing business debt mistakes like extending term without lowering rate or stacking more debt. When you’re ready, get matched with lenders that offer refinance or consolidation.

Decision Framework and Underwriting Reality

Execution Checklist Before You Commit

- Data consistency: application figures align with statements and debt schedule.

- Payment fit: projected payment works in low-cash months.

- Structure fit: term and cadence match customer payment timing.

- Close readiness: signer availability, entity docs, and bank verification are ready.

Post-Funding Controls for Better Future Terms

Advanced Planning: Cost, Cadence, and Contingency

Governance and Team Alignment

Deep-Dive Playbook for Sustainable Liquidity

Metrics to Track Monthly

- Deposit trend: rolling three-month average vs prior period.

- Debt-service load: monthly payments relative to inflows.

- NSF events: count and root cause.

- Forecast variance: actual cash performance vs approval assumptions.

Scenario Planning and Cash-Flow Stress Testing

Strong financing decisions are made before urgency peaks. Build three scenarios: base, moderate stress, and severe stress. For each case, map expected inflows, fixed obligations, variable expenses, and debt service. The objective is to identify where payment pressure appears and adjust structure before commitments are signed.

In many small businesses, a 10% to 15% revenue dip combined with slower collections is enough to expose repayment mismatch. If the stress case fails, reduce requested amount, extend term where possible, or choose a structure with greater flexibility. These adjustments are easier and cheaper pre-close than after the first tight month.

Operating Controls That Reduce Financing Risk

- Weekly cash review: compare forecast to actual and document variances.

- Receivable cadence: track top clients and escalation timing for slow pay.

- Vendor strategy: negotiate terms proactively before pressure rises.

- Payment hierarchy: define which obligations remain highest priority under stress.

- Communication protocol: assign one owner for lender and advisor updates.

These controls improve more than daily operations. They also improve underwriting narratives because they demonstrate management discipline. Lenders frequently reward borrowers who can explain controls with evidence instead of general promises.

Offer Comparison Framework

Normalize every offer to three dimensions: total dollars repaid, timing of debits, and flexibility under underperformance. A quote with lower nominal price can still carry higher operating risk if payment cadence collides with your receivable cycle. Likewise, a faster approval is not always better when terms force immediate strain.

Build a side-by-side matrix with amount, term, fees, first payment date, prepayment language, and default triggers. Include operational fit notes (for example, whether payments align to payroll or inventory cycles). Decisions become clearer when commercial and operational factors are evaluated together.

Execution Playbook: From Approval to Stable Repayment

Once approved, shift focus from approval excitement to execution discipline. Confirm net proceeds after fees, verify disbursement account details, and calendar payment dates with internal owners. The first 30 days matter: errors at this stage often create avoidable friction and degrade future lender confidence.

Track three early indicators: average daily balance trend, variance between expected and actual collections, and any missed internal reporting deadlines. If negative movement appears, activate pre-defined controls quickly instead of hoping trends reverse on their own.

Governance for Repeatable Financing Success

Businesses with repeatable financing access run lightweight governance. Keep a monthly financing packet with updated debt schedule, key cash metrics, and notes on major changes. This packet supports renewals, refinancing, and strategic discussions with advisors without scrambling for data each cycle.

Before any renewal or top-up request, run a pre-mortem: what could cause delay, repricing, or decline under current conditions? Address those items first. Pre-mortems protect negotiating position and reduce urgency-based decisions.

Long-Horizon Strategy

Capital decisions should support durable operating resilience. Avoid optimizing for one metric such as fastest closing or lowest first payment. Optimize for sustainable repayment, transparent terms, and options if assumptions change. Over multiple quarters, this approach lowers total financing cost and reduces risk of repeated distress cycles.

When leadership treats financing as an operating system rather than a one-time event, both lenders and internal teams respond with greater confidence. That confidence compounds into better terms, faster processes, and stronger strategic flexibility.

Detailed Checklist for Internal Finance Teams

- Reconcile debt schedule to actual bank outflows in the last 90 days.

- Validate that legal entity names and tax IDs match across all documents.

- Prepare a one-page use-of-funds memo tied to revenue timing.

- Create a rolling 13-week cash forecast with base and stress assumptions.

- List all renewal dates, notice windows, and potential prepayment rules.

- Assign a backup signer so document execution never stalls.

- Document vendor and customer concentration risk with mitigation actions.

- Archive approvals, declines, and lender feedback for future applications.

Running this checklist before each application reduces operational errors and improves cycle time. Even when outcomes are constrained by market conditions, better preparation improves option quality and negotiation leverage.

Extended Operating Playbook

When market conditions shift quickly, businesses that respond with structure outperform businesses that respond with urgency alone. Start by updating your 13-week cash forecast with realistic collection assumptions and revised cost inputs. Then identify actions that can be activated in sequence: tighten discretionary spend, accelerate receivable outreach, and renegotiate vendor timing where relationships permit.

Document these actions as thresholds, not suggestions. For example, if average daily balance falls below a defined level, trigger specific measures within 48 hours. This threshold-based approach prevents decision paralysis and preserves optionality while conditions are still manageable.

Commercial Communication Strategy

Stakeholder communication influences outcomes. Internal teams need one set of numbers and one priority order. External partners need concise, factual updates with dates, amounts, and corrective actions. Long narrative updates without quantified impact usually create confusion and slow cooperation.

For lenders, transparency is a competitive advantage. If assumptions changed since approval, communicate early and propose an updated plan. Proactive communication can preserve trust and improve flexibility compared with last-minute distress requests.

Decision Questions Before Any New Obligation

- Does this payment profile stay safe under moderate stress?

- Can we explain the use of funds in one measurable sentence?

- Do we have documented fallback actions if collections slow?

- Will this obligation improve resilience or only postpone pressure?

Answering these questions with evidence reduces financing regret and improves long-term capital access.

Resilience Layer: Preparing for a Second Shock

Many businesses plan for one disruption and get caught by a second. Build a second-shock plan now: define how you will respond if collections slow again, costs rise again, or a key client delays payment unexpectedly. Include pre-approved actions so execution is immediate, not debated in crisis.

Keep a short contingency memo with trigger metrics, owners, and timelines. Review it monthly. This practice improves leadership confidence, lender credibility, and operational stability when volatility returns.

Final Decision Guardrails

Before accepting any financing, confirm three guardrails: payment remains serviceable in stress conditions, total cost is understood in dollars, and structure aligns with real cash timing. If any guardrail is unclear, pause and resolve before signing.

Practical 90-Day Action Plan

Days 1 to 15: reconcile all obligations, update cash forecast, and identify optional expenses that can be paused without hurting core delivery. Days 16 to 45: improve receivable velocity through tighter invoicing cadence, early follow-ups, and escalation rules for overdue accounts. Days 46 to 90: re-evaluate financing structure based on observed results, then decide whether to refinance, renew, or maintain current obligations.

Throughout the 90 days, maintain one operating dashboard with inflows, outflows, debt service, and buffer levels. Dashboards should be reviewed weekly by leadership so emerging pressure is addressed before it becomes urgent.

Leadership Alignment and Accountability

Assign clear ownership for each action item. Finance owns reconciliation and forecasting. Operations owns execution timing and delivery impact. Leadership owns priority trade-offs and lender communication. Accountability prevents duplicate work and removes ambiguity that slows action.

Document decisions and expected outcomes in brief meeting notes. This record creates institutional memory and improves future financing cycles by showing what worked under real stress.

Bottom Line

Resilient businesses survive volatility by combining disciplined operations with well-structured financing. Focus on cash timing, transparent communication, and realistic commitments. That combination creates better outcomes than chasing speed alone.