The five term loan mistakes that cost thousands: choosing the longest term to minimize payment (a 7-year vs 3-year term on $200K at 8% adds $37,000+ in interest), ignoring origination and doc fees (commonly 1-5%, so $6,000 on a $300K loan), signing without checking prepayment penalties (3-5% of the balance or yield maintenance), failing to compare 3+ lender offers, and borrowing more or less than you actually need. Always compare total repayment — principal plus interest plus fees — not just rate or monthly payment.

1. Choosing Term Length by Payment Alone

The longest term often has the lowest monthly payment, but it also means more total interest. On a $200,000 loan at 8%, a 3-year term might cost roughly $25,000 in interest, while a 7-year term could cost $62,000 or more—over $37,000 in extra interest for the same principal. Choosing a 7-year term just to get a lower payment when you could afford a 3- or 5-year term is one of the costliest term loan mistakes.

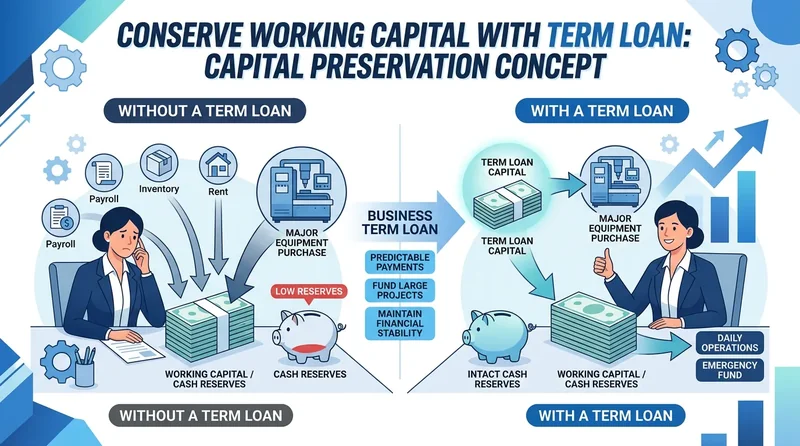

Match the term to how long you need the funds and how quickly you can repay. Use a loan calculator to compare total interest at different terms. If your cash flow supports a shorter term, take it and save. See how much you can qualify for with a business term loan and what lenders look for so you can structure the loan to your advantage.

2. Ignoring Origination and Other Fees

Term loans often include origination fees (1-5% of the loan amount), documentation fees, and sometimes annual or monthly account fees. A 2% origination fee on a $300,000 loan is $6,000 upfront. Add other fees and your effective cost is higher than the stated rate. Comparing only the interest rate across lenders can mislead you when one lender has low rate but high fees and another has a slightly higher rate but no origination fee.

Request a full fee schedule and an APR or total-cost disclosure that includes all fees. Compare total amount repaid (principal + interest + fees) across offers. See secured vs unsecured business term loans for how structure affects rate and fees.

3. Signing Without Understanding Prepayment

Many borrowers assume they can pay off a term loan early to save interest. Some loans have prepayment penalties that make early payoff expensive—e.g., 3-5% of the remaining balance, or yield maintenance that compensates the lender for lost interest. If you refinance or pay off early to capture lower rates or free up cash flow, a large penalty can erase the benefit.

Before signing, ask: Is there a prepayment penalty? How is it calculated? Is there a lockout period? Get it in writing. If you expect to pay early, choose a loan with no prepayment penalty or a declining penalty, even if the rate is slightly higher. See how to avoid overpaying on equipment financing for the same principle on other products.

4. Not Comparing Multiple Lenders

Rates and terms vary widely. Accepting the first offer without shopping can leave thousands on the table. Use a single application through a marketplace or broker to get multiple term loan offers so you can compare rate, term, fees, and prepayment in one place. Get matched with business term loan lenders to compare without multiple credit pulls.

5. Borrowing More or Less Than You Need

Borrowing more than you need increases interest and fees for no benefit. Borrowing too little can force you to come back for a second loan (another round of fees and credit impact) or to use high-cost short-term financing to fill the gap. Model your need carefully and borrow the right amount for the right term. See when a business term loan is not the right option so you do not use a term loan when a line of credit or other product fits better.

Summary: Compare Total Cost and Read Prepayment

Term loan mistakes that cost thousands usually come from wrong term length (too long for the need), hidden fees, and prepayment penalties. To avoid them: compare total cost (principal + interest + fees), not just payment; get a full fee schedule and APR; understand prepayment before you sign; compare multiple lenders; and borrow the right amount. When you are ready, get matched with business term loan lenders who offer clear terms and competitive rates.

Consistent monthly monitoring turns a good term sheet into a durable financing outcome over the full repayment cycle.

Frequently Asked Questions

What is the biggest term loan mistake?

Choosing a term based only on monthly payment. A longer term lowers the payment but increases total interest paid—sometimes by tens of thousands of dollars. Always compare total cost (principal + interest + fees) over the life of the loan and match the term to how long you need the funds.

Do business term loans have prepayment penalties?

Some do. Penalties can be a percentage of the remaining balance, yield maintenance, or a lockout period. Before signing, ask if there is a prepayment penalty and how it is calculated. If you may pay early, negotiate no penalty or a declining one.

What hidden fees should I look for in a term loan?

Origination fees, documentation fees, processing fees, and annual or monthly account fees can add 1-3% or more to your cost. Request a full fee schedule and an APR or total-cost disclosure that includes all fees so you can compare offers fairly.